New car registrations continue their dive (Update)

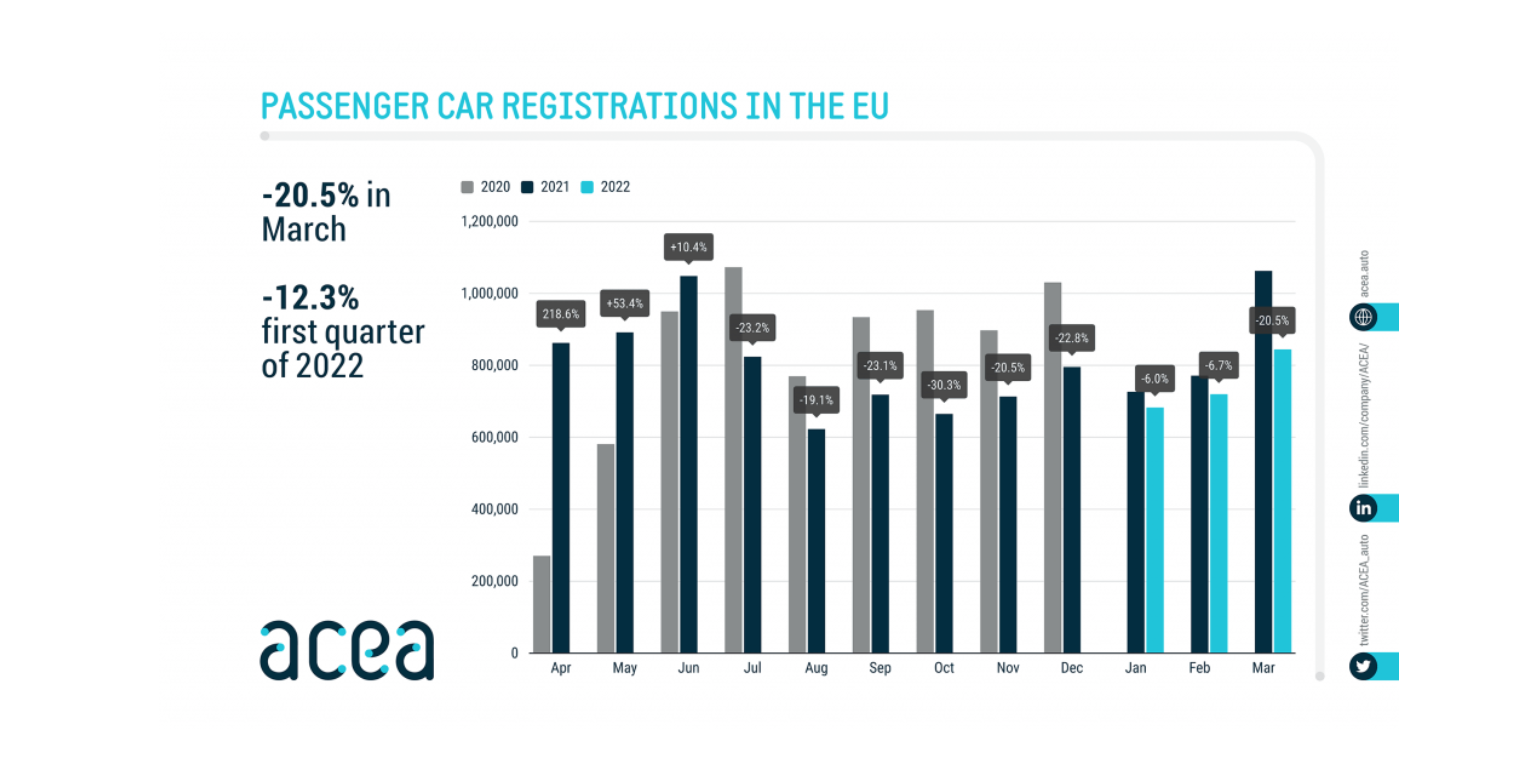

Sales figures are declining all over Europe, ACEA’s statistics confirm. The record low sales are due to the war in Ukraine and the persisting shortage of semiconductors /ACEA

During the first quarter of 2022, 103 146 new cars were registered in Belgium, 13,5% less than in 2021. The same pattern can be seen all ove

Comments

Ready to join the conversation?

You must be an active subscriber to leave a comment.

Subscribe Today