European car sales: growth and electrification continue

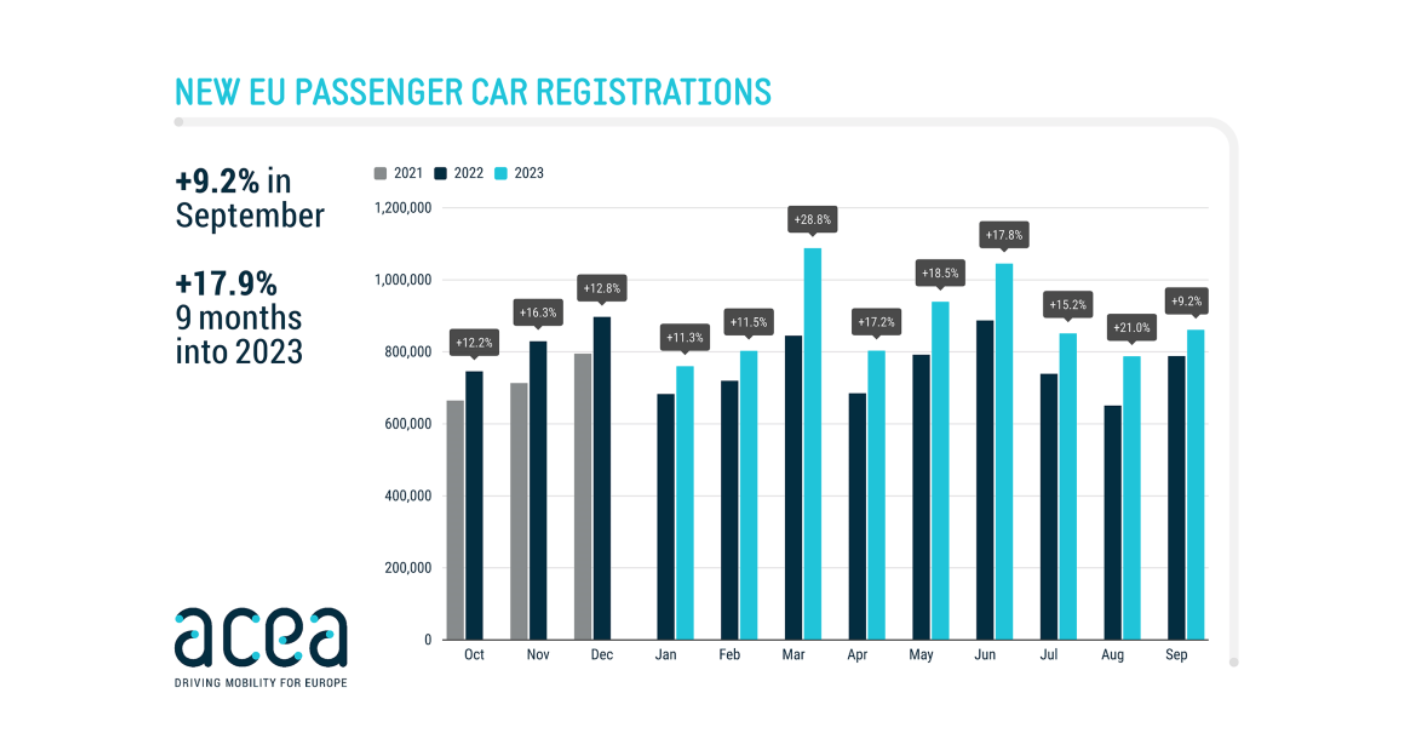

According to figures coming from ACEA, the EU market grows for its 14th consecutive month. Pre-pandemic results, however, stay far out of reach /ACEA

New figures from the European Car Manufacturers Association ACEA indicate that the European car market has seen a 14th consecutive month of

Comments

Ready to join the conversation?

You must be an active subscriber to leave a comment.

Subscribe Today