EU car registrations: EV surge slows down

Compared to a weak January 2023, the EU car market progresses, but in general, the market forecast is not rosy, surely not for electrified vehicles /ACEA

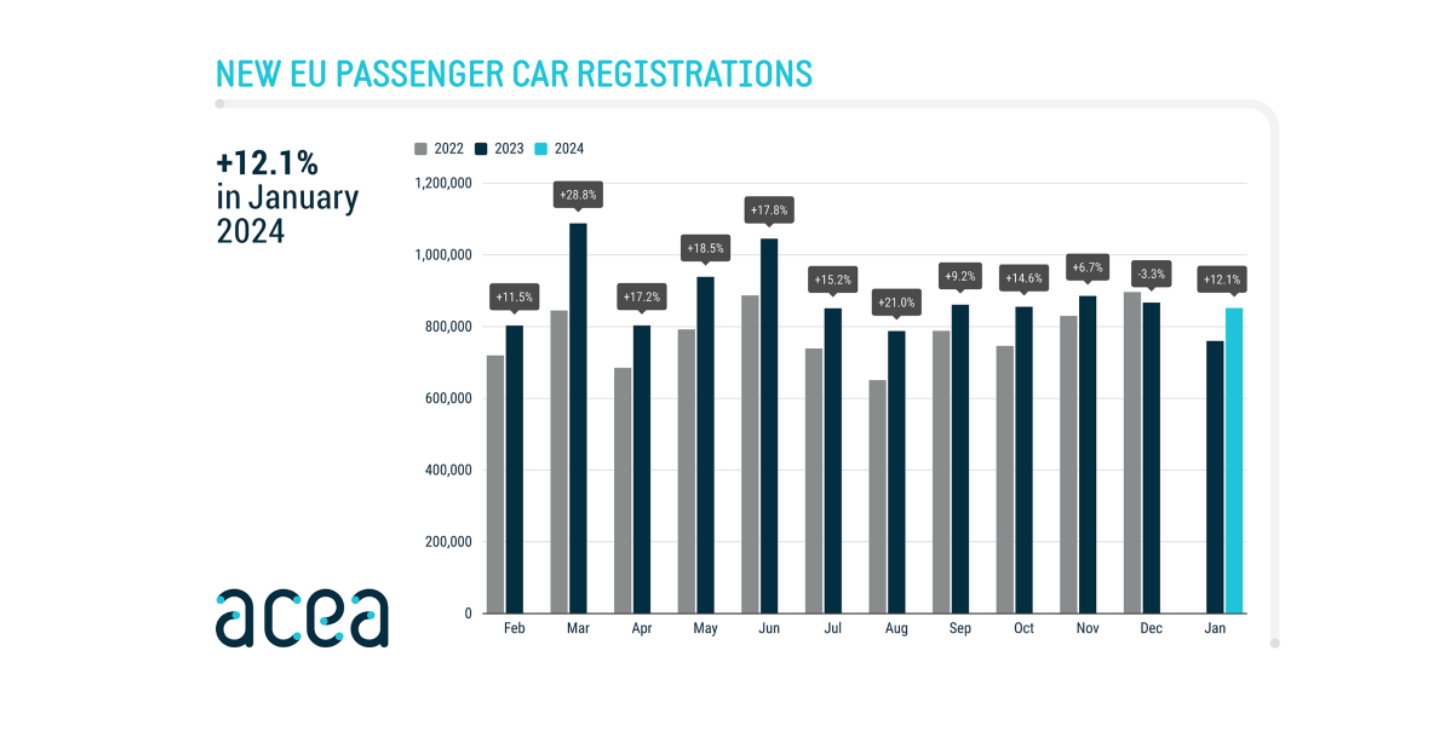

According to the data of the European Car Manufacturers Association ACEA, the EU new car market in January 2024 rebounded from the slowdown

Comments

Ready to join the conversation?

You must be an active subscriber to leave a comment.

Subscribe Today